Carbon Masters

-News & Events

+44(0)1912902717 9:30 - 17:30 (GMT) +91-9148923921

Nov 4 2025

Blog

Turning Digestate into Value: FOM, LFOM, and the Commercial Journey of Soil Carbon Solutions.

Introduction: The Soil Carbon Imperative

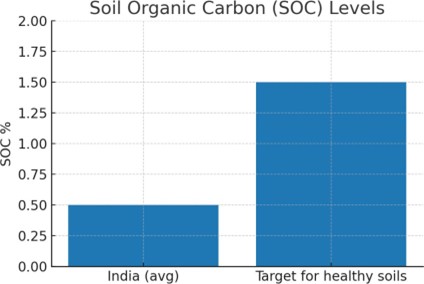

Indian agriculture faces a looming soil carbon crisis. Decades of intensive farming, indiscriminate use of chemical fertilisers ,particualry Urea , and declining use of farmyard manure have left soils depleted of organic carbon. Current soil organic carbon (SOC) levels across much of India average below 0.5%, far short of the 1.5–2% needed for healthy, resilient soils. Low SOC translates into declining productivity, weak water retention, and reduced resilience to climate stress.

Soil Organic Carbon Levels

Figure 1 : Average soil organic carbon (SOC) in Indian soils compared with the target range for healthy soils.

Against this backdrop, the emerging compressed biogas (CBG) sector presents a unique opportunity. Every tonne of biogas produced from organic waste leaves behind a nutrient- rich slurry, or digestate. Managed correctly, this digestate can be converted into high- quality organic fertilisers that restore carbon to soils while providing farmers with nutrient- rich, sustainable alternatives to chemical fertilisers. The two most prominent forms of processed digestate in India’s regulatory framework today are Fermented Organic Manure (FOM) and Liquid Fermented Organic Manure (LFOM).

The commercial journey of FOM and LFOM is inexorably linked to the viability of CBG projects themselves. Monetising the organic output is as critical as selling the gas: a CBG plant that fails to capture value from digestate risks becoming financially unsustainable.

FOM and LFOM: The Opportunity from Digestate

Digestate management is the linchpin of a successful CBG project. Roughly 90% to 95% of the feedstock input to an anaerobic digester exits as slurry. If this output is poorly handled, it poses an environmental liability; if processed effectively, it becomes an agricultural asset.

- Fermented Organic Manure (FOM): A solid organic fertiliser derived by dewatering digestate and curing it with bulking agents such as garden waste. Rich in organic matter and nutrients, FOM directly contributes to increasing soil carbon levels while supplying essential NPK (nitrogen, phosphorus, potassium).

- Liquid Fermented Organic Manure (LFOM): The liquid fraction of digestate, which can be applied to soils or used in fertigation LFOM provides soluble nutrients and organic acids, acting as a soil conditioner and microbial stimulant.

Together, FOM and LFOM close the nutrient loop in agriculture: organic waste is transformed into renewable energy (CBG) and carbon-rich soil inputs.

The Commercial Lens: Why Digestate Matters for CBG Success

The commercial journey of a CBG plant is often told through the lens of gas sales. However, digestate monetisation is equally critical.

- For every 10 tonnes of feedstock processed, a plant may produce 1–4 tonnes of solid FOM and thousands of litres of LFOM.

- The revenue from digestate products can contribute 20–30% of total project

- Without a structured outlet for digestate, plants incur costs in storage, disposal, or transportation—quickly eroding profitability.

Thus, the long-term success of the CBG industry depends not only on securing offtake agreements for gas but also on innovating in digestate processing and marketing.

Government Support: The MDA Scheme

Recognising the role of organic fertilisers form CBG plants in improving soil health, the Government of India introduced Market Development Assistance (MDA) to support the sale of FOM and LFOM. Under this scheme, CBG producers can claim a subsidy to partially offset costs of processing, and distributing digestate-based fertilisers.

The scheme represents a crucial first step in mainstreaming digestate utilisation:

- It gives CBG producers a financial cushion to commercialise FOM and

- It aligns the CBG sector with the national mission of improving soil health and reducing chemical fertiliser dependency.

Early Challenges in FOM and LFOM Registration

While MDA support has been a welcome development, the industry’s initial experience has highlighted practical hurdles:

- Registration: CBG producers must register FOM and LFOM products with the fertiliser regulatory The process requires product testing, certification, and compliance with FCO (Fertiliser Control Order) standards—often a lengthy and bureaucratic exercise not helped by frequent Portal-related Challenges: Frequent technical issues and user difficulties with platforms like the IFMS and GOBARdhan portals have hindered smooth registration, reporting, and MDA claim submissions.

- Inter-agency Awareness Gaps: Many state-level agriculture departments and local officials were initially unfamiliar with digestate-based fertilisers, leading to delays in acceptance and certification. We’ve observed a lack of coordination between central ministries and state departments, leading to delays in approvals, inconsistent enforcement of norms, and confusion over roles and responsibilities.

- Distribution Bottlenecks: Even with registration, producers faced challenges in building farmer awareness, distribution networks, and convincing farmers to shift from heavily subsidised chemical fertilisers.

These challenges slowed the initial uptake but also underscored the need for a more robust policy and market ecosystem for digestate-based fertilisers.

While MDA Support is welcome , by itself its Not Enough

While MDA provides important short-term relief, it is not a long-term solution. For several reasons:

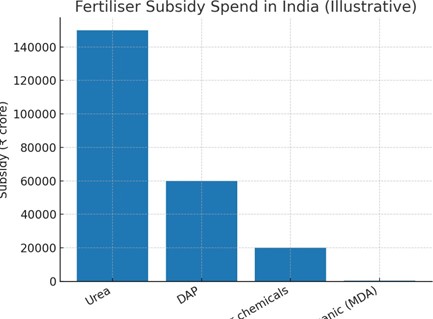

- Scale of Subsidies: MDA support is limited in scope compared to the vast subsidies available to chemical fertilisers such as urea and ( Figure 2 )Competing on price without innovation will be difficult.

Figure 2. : Illustrative comparison of government subsidy expenditure on chemical fertilisers vs. organic (MDA). The imbalance underscores why innovation in digestate-based products is essential for long-term adoption.

- Farmer Adoption: Farmers will ultimately adopt FOM and LFOM not because of subsidies but because they see better yields, improved soil health, and cost savings.

- Innovation Imperative: To win farmer trust and create differentiated products, CBG producers must innovate beyond basic FOM and LFOM.

The Path Forward: Innovation in Digestate Products

This is where we at Carbon Masters are headed. By rethinking digestate management, we are developing premium products better tailored to farmer needs:

- Carbonlites Bio-Enriched Organic Manure: By combining digestate with composted garden waste and microbial biofertilisers, Carbonlites improves nutrient availability particularly carbon , soil water retention and builds resistance to pests

- Two further product initiatives are currently under development.

Firstly A Phosphate-Enriched Organic Fertiliser which can replace India’s dependence on imported DAP. Enriched digestate products can partially substitute for phosphate fertilisers, reducing subsidy burdens and foreign exchange costs.

Secondly a Biochar-Enriched Organic Fertiliser. Blending biochar into digestate-derived manure enhances carbon sequestration, improves soil structure, and locks carbon in soils for the long term.

These innovations move beyond commodity FOM and LFOM, creating value-added fertilisers that deliver tangible benefits to farmers and measurable carbon outcomes for policymakers.

Conclusion: A Dual Opportunity for CBG and Indian Agriculture

The Indian CBG industry is not just about replacing fossil fuels with renewable gas. Its success depends equally on how well it harnesses the potential of digestate. FOM and LFOM represent the first steps on this journey—critical products that can restore soil carbon, provide sustainable alternatives to chemical fertilisers, and monetise the by-products of gas production.

However, MDA support, while useful, is only a bridge. The long-term viability of digestate management lies in innovation—creating differentiated, farmer-friendly, and carbon- positive products. Carbon Masters’ work with Carbonlites bio-enriched organic manure, phosphate substitutes, and biochar-enriched fertilisers shows the direction in which the industry must move.

In doing so, the CBG sector can become a cornerstone of India’s soil carbon regeneration strategy. Utilising digestate effectively is more than waste management—it is a once-in-a- generation opportunity to rebuild soil health, strengthen food security, and deliver on India’s climate commitments.

About Carbon Masters

Carbon Masters is a Bangalore based climate tech company that has pioneered the conversion of the organic fraction of MSW into its two climate friendly brands: Carbonlites biomethane and Carbonlites bio enriched organic manure . It builds and operates Carbonlites CBG plants across three states in India selling its gas to the hospitality sector to displace LPG, to Bunks and CGD networks to replace CNG and to industrial customers aiming to get to net zero emissions. Its sells its Carbonlites Organic fertilser to farmers via FPO’s and agricultural dealers

About Carbon Masters

Carbon Masters is a carbon management consultancy which helps organisations in the public and private sector to measure, manage, reduce and report their carbon emissions.